FY25/26 Budget Review: High stakes in a ‘priced for perfection’ economy – a balancing act

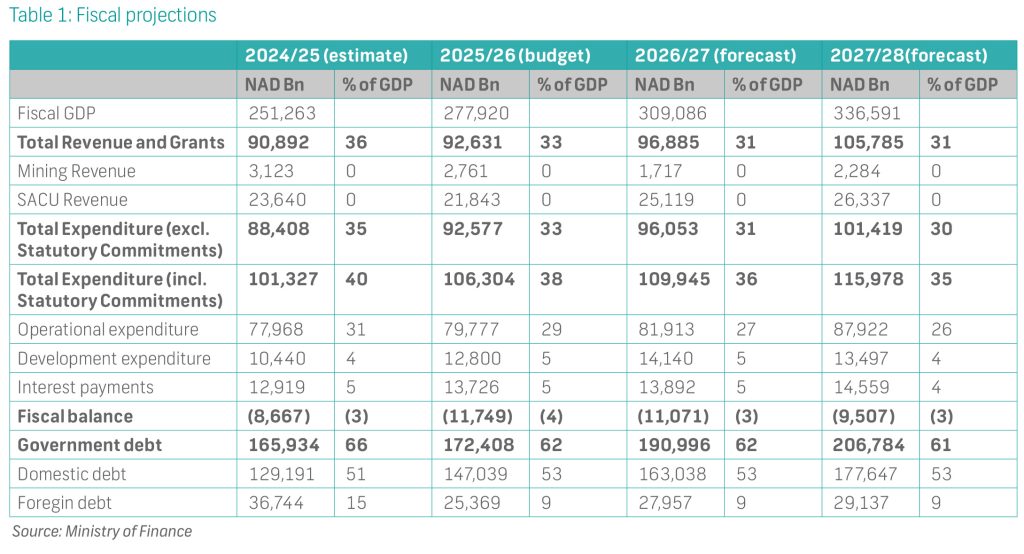

- • The Ministry of Finance (MoF) expects GDP growth to reach 4.5% y/y in 2025 and 4.7% in 2026, up from 3.7% in 2024. This is anticipated to be supported by a strong mining sector performance, favourable commodity prices, and increased exploration activity amid easing inflationary pressures.

- • Fiscal revenue is expected to rise to NAD92.6bn in FY25/26 from the MoF’s revised estimate of NAD90.9bn in FY24/25, supported by higher GDP growth figures.

- • New tax reforms include a reduction of the non-mining corporate tax rate to 28% by FY26/27, a 10% dividend tax effective from January 2026, and e-invoicing for VAT to improve compliance. Individual income tax brackets will be adjusted for inflation, providing relief to the working class of NAD712.9m annually.

- • Total expenditure is projected at NAD106.3bn for FY25/26, representing a 4.9% increase from the revised FY24/25 estimates.

- • Development expenditure is projected at 4.6% of GDP, reflecting a 22.6% increase from the previous year.

- • The fiscal deficit is expected to widen by 29.9% to NAD12.8bn (4.6% of GDP) in FY25/26, due to Southern African Customs Union (SACU) and mining company taxes, which are likely to come under pressure.

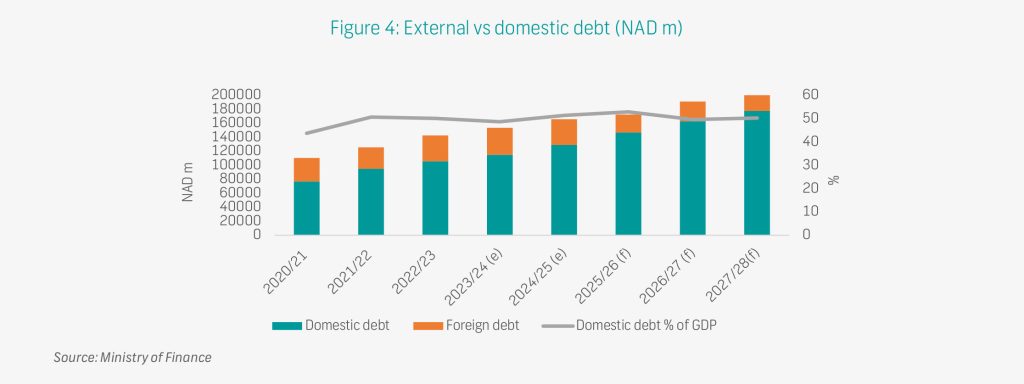

- • The total debt stock is projected to reach NAD172bn (62.0% of GDP) in FY25/26, with 85% of the debt being domestic.

- Interest expenditure is set to increase by 6.2% to NAD13.7bn, constituting 14.8% of total revenue.

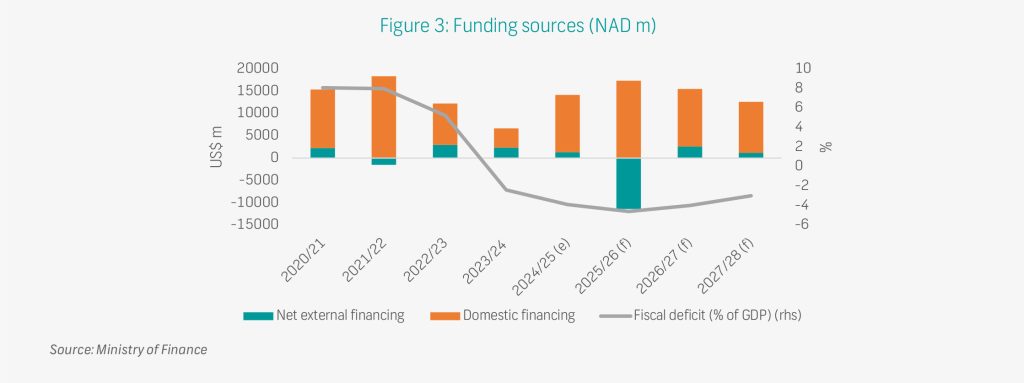

- • Domestic issuances will be heavily relied upon, with domestic financing expected to amount to NAD17.3bn — the second- largest domestic financing requirement in Namibia’s history.

Economic Backdrop: Weaker growth prospects

On 27 March 2025, the newly-appointed Minister of Finance, Erica Shafudha, tabled the National Budget for the 2025/26 fiscal year. At the time of publication, the finalisation of the National Budget was still underway, primarily due to ongoing adjustments involving the reallocation and renaming of votes. As a result, the full set of budgetary data was not yet complete. While these changes are expected to be minor, they may lead to discrepancies between the figures currently available and those that will ultimately be debated in parliament.

This note will be updated and reissued with amended figures once the finalised data becomes available. For this publication, we have used the fiscal tables as revised and published on the Ministry of Finance’s website on 27 March 2025.

The Ministry of Finance (MoF) has marginally revised its global and regional growth projections upward from the FY24/25 mid- year budget review tabled in October 2024, referencing the January 2025 World Economic Outlook (WEO) projections for global growth (3.2% in 2024 and 3.3% in 2025) to be sluggish and well below historical averages of 3.7% and reflecting persistent global challenges, including weak consumption and policy uncertainty. Sub-Saharan Africa’s growth is expected to improve from 3.8% in 2024 to 4.2% in 2025, driven by resilient regional activity despite climate shocks. This marks a notable upward revision from the previous estimates of 3.5% and 3.9% for 2024 and 2025, respectively, tabled in the FY24/25 mid-year review, reflecting improved optimism in the region’s primary sector output.

Domestic GDP growth is projected at 4.5% in 2025 and 4.7% in 2026 by the MoF, the highest among consensus views, primarily driven by a strong mining sector performance due to favourable uranium and gold prices and continued exploration activity. Exploration companies have signalled a final investment decision within the Medium-Term Expenditure Framework (MTEF) by 2027. Additionally, growth is expected to be supported by normalised rainfall patterns that will boost agriculture, improved consumer confidence from tax relief measures, and a more accommodative monetary policy stance, which benefits the wholesale and retail sectors. While not implausible, we view these forecasts as optimistic. Any unforeseen economic shocks could place significant pressure on the government’s elevated fiscal assumptions, particularly with respect to the debt-to-GDP and deficit-to- GDP ratios.

Global inflation is expected to moderate but at a slower pace than previously anticipated. Energy prices are projected to decline in 2025, driven by subdued demand from China and increased oil production by non-OPEC members. The impact of United States (US) President Donald Trump’s “Liberation Day” tariffs remains uncertain, and its consequences for global trade are dependent on the extent of the tariffs.

Despite easing inflation, global uncertainty around the pace of disinflation has delayed monetary easing in many jurisdictions. The Bank of Namibia (BoN) is expected to maintain a cautious stance in 2025. As a result, credit extension is anticipated to remain subdued, reflecting weak consumer spending and elevated debt servicing costs.

Revenue: Fiscal coffers weighed down by regional and global shocks

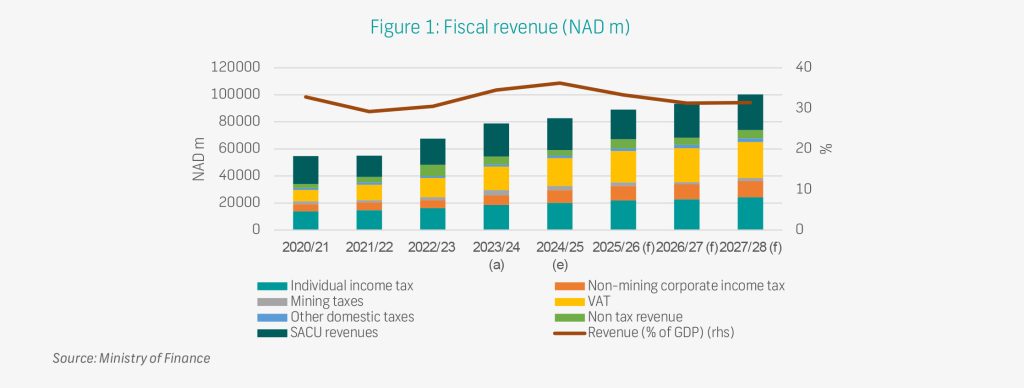

Revenue for FY24/25 is expected to increase by 11.5% from the previous year to NAD90.9bn, driven by higher SACU receipts, VAT, and personal income tax. The anticipated increase is, however, slightly behind mid-year estimates, with revenue being revised down from the NAD92.1bn expected in October 2024. Moving forward, the MoF expects to receive 18.7% more revenue during FY25/26, projecting NAD92.6bn, largely driven by higher non-tax revenue due to an additional NAD1.6bn from the dissolution of the Namibia Post and Telecom Holdings company. Revenue is projected to grow by 4.59% and 9.19% in FY26/27 and FY27/28, respectively, breaching the NAD100bn mark in the latter period.

Revenue expectations, however, remain an area for concern as traditional drivers (diamonds and SACU receipts) remain under pressure and are expected to drop significantly in FY25/26. SACU receipts are expected to drop by 24.1% to NAD21.7bn relative to the previous year and diamond mining company taxes will be lower for a second consecutive year, projected at ~NAD200m

– significantly lower than the NAD2.3bn collected in FY23/24. The sustained downturn in the global diamond industry poses a persistent risk to Namibia’s fiscal revenue, driven by a structural shift in consumer preferences toward sustainability. This shift

is expected to have a lasting impact on global diamond production, limiting the sector’s contribution to the national fiscus. In FY24/25, revenue lost due to lower diamond sales was partially offset by an increase in other mining tax revenue, which moved up from NAD1.6bn to NAD2.8bn; similar (NAD2.6bn) revenue generation from the mining sector is expected in FY25/26. The improvement is largely expected to be driven by elevated production and prices in key commodities such as uranium, copper and gold.

To offset these shortfalls, taxes on domestic goods and services (primarily VAT collections) are expected to increase significantly by 12.0% to NAD25.3bn in FY25/26. This anticipated growth would make non-mining taxes the highest contributor to revenue, accounting for 27.3% of total revenue and surpassing SACU and diamond receipts. Moreover, albeit small, the government has included dividend tax revenue to contribute NAD351m and NAD355m in FY26/27 and FY27/28, respectively.

Revenue expectations over the MTEF are reasonable, albeit ambitious. The reliance on a strong VAT performance presents a notable risk; if VAT collections fall short, due to weaker-than-expected economic growth or collection inefficiencies, this would place strain on overall fiscal targets. However, the probability of this risk materialising appears slightly tilted to the downside given the current macroeconomic conditions and ongoing tax administration reforms.

Tax policy reform: Aimed at enhancing competitiveness

The FY25/26 budget introduces various tax policy reforms aimed at improving domestic revenue mobilisation and enhancing Namibia’s investment climate:

- • The non-mining corporate tax rate will be reduced in a phased manner from 30%, effective 1 January 2025, to 28% by FY26/27. This reduction aims to improve Namibia’s competitiveness and attract greater private sector investment.

- • A 10% dividend tax will be introduced, effective 1 January 2026, as part of measures to broaden the corporate income tax base.

- • The Namibia Revenue Agency (NamRA) plans to roll out e-invoicing for VAT by April 2026 to improve compliance and reduce administrative inefficiencies. This initiative is expected to enhance accuracy, lower administrative costs, and curb VAT fraud.

Expenditure: All about targeted social stimulus

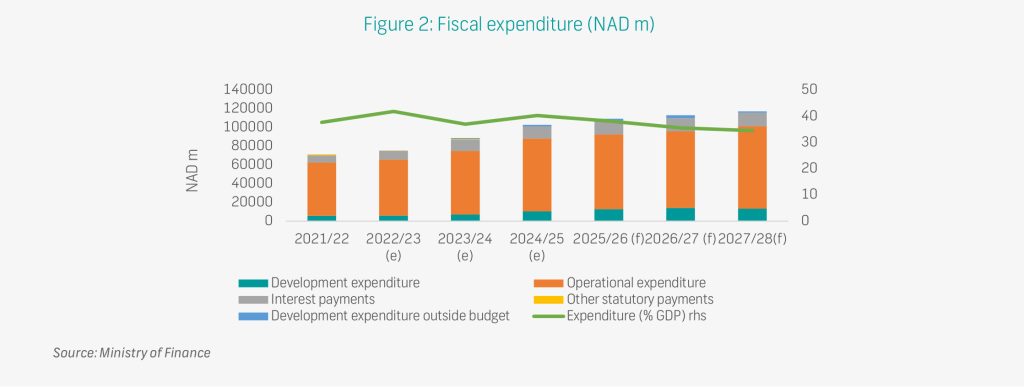

- • In line with our expectations, the FY25/26 budgeted expenditure prioritises sustaining ongoing operations while focusing

on infrastructure development, youth empowerment, and social protection. Total expenditure is estimated at NAD106.3bn

in FY25/26, representing a 4.9% increase from the revised estimates of FY24/25. Current expenditure is now projected at NAD79.8bn, accounting for 75.1% of total spending. This reflects a modest 2.3% increase from the FY24/25 mid-term estimates, largely driven by increased personnel expenditure following adjustments to the civil service wage bill, higher allocations for health and social services, and increased domestic food production and economic development, as reflected in the three main shares of allocations below:

- • Ministry of Education, Innovation, Arts and Culture: NAD24.8bn in FY25/26 rising to NAD76.1bn over the MTEF.

- Ministry of Finance: NAD14.6bn in FY25/26, which includes NAD7.2bn for the various social grants and transfers to SOEs. NAD100.0m was budgeted for the Meat Corporation of Namibia (MeatCo), while NAD320m has been allocated for TransNamib to improve efficiencies, infrastructure development, and overcome operational challenges.

- • Ministry of Health and Social Services: NAD12.3bn in FY25/26 rising to NAD37.5bn over the MTEF. This includes NAD780m in FY25/26 and NAD2.7bn over the MTEF in the development budget for the expansion of health infrastructure throughout the country and pharmaceutical supplies. On the other hand, the government has shown a commitment to capital development. Development expenditure is projected at NAD12.8bn, or 4.6% of GDP, representing a 22.6% increase from the previous year when the development budget was reduced

- due to the administration’s concerns around execution rates. This increase demonstrates the government’s commitment to addressing infrastructure bottlenecks and strengthening confidence in execution capacity.

- In this regard, the development budget in the FY25/26 budget has increased by NAD2.4bn to NAD12.8bn, with the biggest gains allocated to the following ministries:

- • Ministry of Health and Social Services: Increased by NAD323m to NAD780m in FY25/26, reflecting the commitment to improving health infrastructure.

- • Ministry of Sport, Youth and National Service: Allocated an additional NAD386m from FY24/25 to NAD510m in FY25/26.

- • Ministry of Defence and Veterans Affairs: Allocated a NAD600m budget for FY25/26, representing a NAD200m increase from FY24/25.

- • Ministry of Information and Communication Technology: Increased by NAD119.2m in FY25/26 to NAD259.2m, up from NAD140m in FY24/25.

- • External Loan Funded Projects: Allocated the largest increase by NAD1.5bn to NAD3.2bn in FY25/26, up from NAD1.6bn in FY24/25. Lastly, support to public enterprises remains a key fiscal priority, in line with the 2024 Mid-Year Budget Review, with NAD320m allocated to TransNamib to address infrastructure and operational challenges. Meanwhile, dividends from public enterprises are projected to decline in FY25/26.

Fiscal deficit: Financing through the domestic market, but at what cost?

The primary surplus has been revised down by NAD1.3bn to NAD915m (0.3% of GDP) for FY25/26. Thereafter, the deficit is expected to decline gradually to 4.0% and 3.0% of GDP in FY26/27 and FY27/28, respectively. While the increased deficit is anticipated, concerns remain as traditional revenue drivers such as SACU receipts and mining company taxes are likely to come under severe stress over the MTEF. Additionally, Namibia’s deficit outlook, once significantly better than South Africa’s, is expected to normalise over the forecast period, with the two countries likely to run similar budget balances (relative to the size of their economies) —a concerning development given their divergent growth prospects.

In addition to the widening deficit, the large volume of debt obligations maturing in FY24/25 and FY25/26 is expected to add strain on the fiscus. Pension funds, which remain compliant with domestic investment regulations by investing over 50% of their

portfolios locally, provide a stable source of funding. However, the MoF acknowledged concerns over this trend, stating that “Given the prevailing interest rate levels, we believe it is the most optimal to source funding from the domestic market considering the sufficient liquidity levels as well as the demonstrated appetite for government securities”. While domestic funding may be more cost-effective, the impending Eurobond repayment and the reliance on domestic issuances could strain liquidity and slow economic growth.

Lower government balances could ultimately force a slowdown in expenditure, reducing liquidity in the economy, delaying payments to contractors and workers, and potentially impacting the execution rates of the development budget. These factors highlight the growing risks associated with increased reliance on domestic financing, which may lead to further fiscal strain if not carefully managed.

Debt: Interest rate pressures remain

Due to wider financing requirements, Namibia’s total debt stock is projected to reach NAD172bn (62.0% of GDP) in FY25/26, with 85% of the debt being domestic and the remainder sourced externally. The debt composition is expected to remain highly concentrated in domestic debt, reflecting the planned Eurobond repayment in October 2025.

Higher debt levels will push interest expenditure up by 6.2% to NAD13.7bn (14.82% of total revenue) in FY25/26, an upward revision of NAD615m from the mid-term budget. This increase is primarily due to a rise in domestic interest payments, which are expected to climb from NAD10.4bn to NAD11.0bn. However, the government anticipates a decline in domestic borrowing costs in FY25/26, with the effective domestic interest rate expected to fall from 8.53% in FY24/25 to 7.98%, continuing its downward trajectory over the forecast period. Nevertheless, if this assumption does not materialise, it presents an upside risk to expenditure.

The total financing requirement for FY25/26 is estimated at NAD6.0bn, slightly below the initial projection of NAD6.2bn. The

MoF outlined the Eurobond redemption plan for 2025, noting that US$463m has been accumulated in the Sinking Fund over the past financial years. An additional NAD3.0bn (US$162m) is expected to be added in FY25/26, leaving a balance of NAD2.3bn (US$125m) to be refinanced through the domestic market. Furthermore, NAD2.0bn of the FY25/26 SACU receipts will be directed into the Sinking Fund, as per the previous minister’s commitment.

Consequently, the government will rely heavily on domestic issuances to finance the deficit, with domestic financing projected at NAD17.3bn in FY25/26, marking the second-largest domestic financing requirement in Namibia’s history. This reliance presents a significant challenge for government finances, especially given the dampened SACU and revenue outlook, making it unlikely that additional injections will materialise at the anticipated scale. As a result, additional financing needs could surprise to the upside, further increasing fiscal pressure.

Balancing fiscal consolidation, social priorities and infrastructure development

The FY25/26 budget reflects a concerted effort to balance short-term fiscal pressures with long-term developmental goals. While the domestic growth outlook is optimistic — underpinned by buoyant mining activity, favourable commodity prices, and improved consumer sentiment — fiscal sustainability remains a key concern.

The FY25/26 expenditure framework appears broadly reasonable, balancing operational needs with strategic development priorities. The development budget has seen a significant 22.6% increase to NAD12.8bn (4.6% of GDP), signalling renewed confidence in execution capacity and a strong push toward infrastructure investment, youth empowerment, and economic development. While historical execution challenges and pressure on fiscal space pose risks, the expenditure assumptions are well-aligned with national priorities and reflect a pragmatic approach to growth and fiscal sustainability. On the revenue side, projections appear broadly reasonable but are undeniably ambitious. With traditional revenue streams such as SACU and diamond- related receipts under pressure, the fiscal framework leans heavily on a robust VAT performance and broader tax efficiency. Any shortfall in VAT collections—whether due to softer-than-expected growth or administrative inefficiencies—would heighten fiscal risks. That said, the likelihood of this downside risk materialising appears modest, given improved tax administration and favourable underlying economic conditions. The widening fiscal deficit, coupled with a heavy reliance on domestic financing and a looming Eurobond maturity in October 2025, poses liquidity challenges that could limit fiscal space and crowd out private sector activity.

Overall, the budget charts a credible path toward inclusive growth and macroeconomic stability, but its success hinges on walking a very fine line between ambition and realism. The government must carefully navigate competing priorities: stimulating the economy through targeted social and capital expenditure, while maintaining fiscal discipline in the face of mounting pressures.

The widening fiscal deficit, rising debt servicing obligations, and the upcoming Eurobond maturity underscore the limited fiscal space available and the need for prudent debt management. Overreliance on domestic financing could further strain liquidity and suppress private sector credit growth, weakening the very economic foundations the budget seeks to strengthen. At the same time, the effective execution of capital projects and public sector reforms will be critical to sustaining investor confidence and unlocking long-term productivity gains. In this context, the government must balance bold investment with institutional discipline, ensuring that every dollar spent contributes meaningfully to development outcomes. The road ahead will require agility, transparency, and a strong commitment to structural reform to ensure that short-term pressures do not derail long-term progress.

Stay informed with The Namibian – your source for credible journalism. Get in-depth reporting and opinions for

only N$85 a month. Invest in journalism, invest in democracy –

Subscribe Now!